Where a property is subject to a condition which stipulates that it may not be sold, alienated or transferred without the consent of the Home Owners Association of which the owner of the property is a member, the Deeds Office will not register the transfer without the said consent being lodged. Some Home Owners Associations are not active and do not hold meetings.

In order to obtain the required consent it will then entail approaching every registered owner who is a member of the association to sign the required consent. If you are a member of such a non-active association you are advised to take the necessary steps to ensure that it becomes operational and starts to meet in order to prevent the onerous requirement of having to approach every owner to consent in the event of the sale of your property.

Whose Common is it anyway?

We are often approached by members of the public wanting information on common open spaces in specific residential or commercial areas. Questions mostly relate to ownership, maintenance and safety and although we see these areas all around us in our cities, we are not often aware of the legislative rules and regulations attached thereto. More often we receive calls from prospective developers or land scouts with ambition to obtain title to the whole or certain parts of such common space, which of course poses the question: How do these pieces of land fall within the general land use and planning structure and is there any possibility of all such land being developed one way or another in the future?

By way of example specific mention will be made to the Rondebosch Common in Cape Town, as this is a relatively prominent piece of open municipal space attracting huge amounts of interest due to its location and proximity.

The Rondebosch Common was demarcated as lot 17 on the map of Church lands prepared by Surveyor HM Shaw in 1909 and which demarcation was entrenched in the Rondebosch Church lands Act No 27 of 1909 (“the Act”). The land was allocated to the Municipality of Rondebosch under Deed of Transfer 1912 for use by the minister of the Rondebosch St Paul’s Church, but subject to the conditions of the Act mentioned above.

The preamble of the Act provides specifically that this open space “shall at all times remain open to the public as a place of exercise and recreation.” The Act further made provision in s16 for the management and control function to vest with the Municipal Council of Rondebosch and Mowbray for the “purpose of public parks and recreation grounds for thoroughfares…” It will be seen from s14 of the Act that prohibition was placed on alienation in any manner or form, but that the Council had entitlement in terms of s18 to use any portion of the land made inalienable by the Act for increasing the width of or for extending any road shown on the General Plan related or adjacent to this municipal area. This Act was repealed and replaced by Ordinance 19 of 1967 but which ordinance secured the provisions of the Act under title.

On 29th September 1961 the Rondebosch Common was proclaimed a Natural and Historical Monument by the then Minster of Education, Arts and Science at the time, B J Vorster, on application by the Commission for the Preservation of Natural and Historical Monuments, Relics and Antiques. This means that not only is this land subject to the provisions of the Act mentioned above, but also to the provisions of the Natural and Historical Monuments Act 4 of 1934. This would obviate the degree of care with which the Council reached management and control decisions and would further protect the public’s rights to enjoy the free open space.

Bridget O’Donogue, the principle Environmental Planner at the City of Cape Town’s Plumstead Office, confirms that ownership in all such landnow vests with local municipalities and as such, the Rondebosch Common is zoned as a Provincial Heritage Open Space Site. This level of zoning dictates that application for subdivisions on such land, for either municipal purposes or development purposes, is dealt with and assessed by all departments within the City of Cape Town Municipality, including Heritage Western Cape. factors which are taken into account could include but are not limited to heritage and public value, traffic provisions, water and sewerage provisions.

Should the Municipality therefore wish to sell off sections or the whole of the Rondebosch Common, application would need to be tendered to all sections of Council for consideration. The normal transfer procedure would then apply and the Title Deed would be adjusted in respect of removal or insertion of restrictions and further conditions. The Property Management Department of the City of Cape would act representatively should land be sold off for public development or private use.

A concern that certain adjacent homeowners often raise is the one of possibility of future low-cost or government housing on such common open spaces. The Town Planning Department however confirms that these types of applications by government would be viewed through the same process as public applications, which means that the same principles would apply when assessing the validity or viability of such applications.

With reference once again to the Rondebosch Common, it is important to note how previous applications for development were dealt with. In the early 1990s the Council’s Town Planning Branch in conjunction with Council’s Surveys and land Information Branch identified the Rondebosch Common as a “possible site for redevelopment”, with special reference to “low cost redevelopment”, and submitted their Memorandum to the following municipal departments for comment: - City Electrical Engineer, Traffic Manager, City Drainage and Sewerage Engineer, Director of Parks and forestry, City Water Engineer, Director of Building Survey and the Director of Metropolitan Transport Planning. All departments lodged their consent with only one department disagreeing with the suggestion. The Director of Parks and forests rightly pointed out in his reply letter dated 26 January 1995 that “it must be remembered that the Rondebosch Common is a National Monument” and as such the Director confirmed that his department will not consent to any “development of any nature… to be considered…” The Common therefore survived to live another day. Although this answer would not put all property owning neighbours at ease, it does at least reassure that some processes exist for any rezoning on these types of land and proves that these applications are not taken lightly. By the same token, The Heritage Department confirms that, should unlawful occupation occur on open heritage spaces, officials would deal with the eviction procedure under normal legislative provisions.

The Rondebosch Common has however for years been utilised by organisations such as The Rotary Club of Rondebosch and the Ratepayers Association of Rondebosch to stage fundraising and community projects. Should such an event be planned by an organisation, application should be brought to the Town Clerk of the Cape Town City Council who in turn will submit the proposal to all the divisions for approval. Such approvals are readily granted as it would further the object of the Common, as originally envisaged in 1909.

Members of the public cannot as readily obtain copies of title deeds to this land at the Deeds Office as one could for privately owned property, and it would take a considerable amount of investigation to locate the relevant title at the different Council divisions. One needs to apply through the Property Management Department for copies, should inspection or enquiry be necessary.

With regards to the practical management of the Common, it is of interest to know that the Rondebosch Common is maintained by the City Parks department of the municipality and the maintenance relates to grass cutting, refuse removal, tree felling and the general appearance of the site. For any member of the public concerned about the level or standard of upkeep relating to the Rondebosch Common, reference can be made to the list of maintenance regulations which was published in the Province of Cape of Good Hope Provincial Gazette dated 14 August 1919 and which makes specific mention of all Council’s maintenance obligations. Once again, the Property Management Department can be contacted should one require a copy of such list of obligations.

The overall impression which is created by the Planning and Heritage Departments is that these common sites are becoming increasingly valuable for Council, although the value might not always be determined in financial terms but rather more holistically. With big metropolis such as Cape Town and Johannesburg developing at a rapid rate, it is a comfort to believe that our children and their children might still have well-managed, accessible green patches in which to play, something we might have taken for granted in years gone by and well worth preserving.

The “tax amnesty” introduced by SARS (originally Para 51 and now Para 51A of the 8th Schedule of the Income Tax Act) which allows an “amnesty” to homeowners to transfer properties in which they “ordinarily resided” from a CC, Company or Trust, free of transfer duty, capital gains tax and secondary tax on companies, has been written about extensively.

Although there is a little confusion amongst the general public, it can be confirmed that the “amnesty” period for homeowners to use the Para 51A legislation will only expire at the end of December 2012.

CONDITIONS OF THE AMNESTY

There are two important conditions imposed by the current Para 51A in order for you to be able to get the benefits of this type of “tax free” transfer:

- You must have “ordinarily resided” in the property and

- You must have used the property for “mainly domestic” purposes.

The “mainly domestic” provision relates to the requirement that you must not have used more than 50% of the property for business purposes. Simple enough.

However, the requirement that you must have “ordinarily resided” in the property has caused problems since SARS Guidelines have concluded that the property must then have been your “primary residence”. As a result of objection and recommendations, SARS has recognised that this interpretation might be unduly restrictive since this “amnesty” was introduced to all taxpayers to restructure their affairs in the light of changes in the tax laws.

GOOD NEWS FOR HOLIDAY HOME OWNERS!

As a consequence, a Taxation laws Amendment Bill has been introduced for public comment which seems to remove the “ordinarily resided” provision, making it possible, if the legislation is approved in its current format, that second dwellings used by family members and holiday homes will also be able to be transferred in terms of the “amnesty”. If the Bill proceeds through Parliament in the normal way, it would likely be passed in October or November 2011.

Homeowners insurance – Why do we need it?

When you apply for a home loan to purchase a property you will find that the bank will impose the condition that you take out homeowners’ insurance cover for the structure. Why do the banks insist on this cover and why is it so important to understand your policy?

WHAT IS IT?

Homeowners Cover is short term insurance that protects your house and all other permanent structures, improvements and buildings on the property against loss and damage.

WHY DO I NEED IT?

As a homeowner, you should always take into account the possibility that something unexpected like a fire, theft or accident could happen at any time. The best way to ensure that you are protected against such possibilities is through a Homeowners Insurance Policy. Not all homeowners’ policies are the same; therefore you need to ensure that the policy chosen provides the coverage you require.

WHO PROVIDES IT?

All the major banks provide their clients the option of taking the bank’s homeowners’ insurance policy, which would include all the clauses required by the bank to fulfil its own insurance policy requirements. Alternatively, the banks offer clients the option of taking their own homeowners’ insurance – more on this later.

WHAT IS COVERED?

Homeowners’ insurance policies usually include cover for the physical structure, fixtures and fittings like built-in appliances, sanitary ware, geysers, etc. Types of events which are usually included in homeowners’ insurance policies are natural disasters such as floods, lightning and storms, as well as non-natural disasters such as fire, explosions and other accidental damages. However, make a point of reading the policy for exclusions and add on any eventuality which might require cover.

HOW TO CHOOSE A POLICY:

When choosing a homeowners’ insurance policy, keep these very important points in mind:

- avoid looking at the amount of the premiums only as the conditions, inclusions and exclusions of the policy are of equal importance;

- opt for cover equivalent to the replacement value of your home as opposed to the value of your bond;

- due to property value increasing over time, review the sum insured often enough to avoid being under-insured.

ESSENTIAL POINTS TO INCLUDE IN YOUR POLICY:

Where a client has chosen their own insurance policy, and where the property is bonded, the bank will require that the policy conforms with the bank’s requirements before it will be accepted. Each bank differs with their insurance requirements for clients opting for their own insurance. Make sure that you’ve included the following important points in your policy:

- confirmation of the insurance company’s name;

- that the property is insured for the amount determined by the bank;

- confirmation of the property insured;

- the date of inception of the policy must be reflected;

- confirmation of the insurance premium;

- the policy number to be noted on the policy;

- the bank’s interest in the insured property must be noted;

- the bank’s interest must rank prior to your interest;

- that the policy will not be invalidated by any act or omission of yours if such act or omission occurs without the bank’s knowledge;

- confirmation that Sasria cover and Public liability Cover are included;

- confirmation that Subsidence and landslip cover, limited to the sum insured, is included in the policy where insisted by the bank and included in the home loan conditions;

- that the insurance company will take reasonable steps to notify the bank of changes affecting the policy during the duration of the agreement as well as failure on the part of the insured to pay the premiums.

Homeowners’ insurance is one of the most important insurance policies to have in place to ensure that you are adequately covered when unforeseen events occur. Make sure that you choose the best option for you, and make sure that you understand it!

WATER CERTIFICATES: A NEW TRANSFER REQUIREMENT

A new by-law published by the City of Cape Town (section 14 of 2010) now requires the Seller in a property sale transaction to submit a water certificate to the City before transfer of a property in order to obtain rates clearance. The date of implementation is still uncertain.

This “water certificate” is similar to the electrical and gas certificates already required and basically requires an accredited plumber to certify that:

- the water installation conforms to the National Building Regulations

- there are no defects

- the water meter registered

- there is no discharge of storm water into the sewerage system

This however does not mean that the Seller is obliged to carry the costs of having such certificate issued and is a matter that can be negotiated between the Seller and the Purchaser.

It remains to be seen what impact this new requirement will have on the transfer process, but the general feeling in the conveyancing world is that it will not be a positive one. The definition of the term “water installation” and its required conformity to the National Building Regulations will no doubt create countless problems for Sellers trying to sell their property, this biggest being a financial burden when it comes to costs.

It is therefore strongly advise that any potential Seller takes this new requirement very seriously and consult with their attorney before entering into any potential sale agreements.

In most metropolitan areas many properties have undergone a change in use and are no longer utilised as originally intended. In many instances the shift away from the Central Business District area has resulted in former residential areas being utilised for business and other purposes.

It is necessary to comply with the applicable Zoning Scheme Regulations regulated by the Municipality in question. Prior to the purchase of a property a cautious purchaser will require proof of the current zoning from the seller. Additionally confirmation should be sought that any conditions imposed in an approved zoning have been complied with by the seller. From a practical perspective it is usually necessary to seek professional assistance from a person well versed with property law.

Certain conditions imposed by the Municipality when approving a zoning application may carry significant financial implications for a purchaser. In most instances the Municipality imposes a Transport Development Levy (TDL) which requires a substantial payment to the Municipality as part and parcel of a rezoning approval.

In many cases former residential properties are advertised and sold as business sites. In certain cases no formal rezoning application has in fact been prosecuted to the Municipality and the property simply falls within an area where a business zoning may be supported by a Municipality "in principle". However until such time as a rezoning application has in fact been successfully prosecuted and the conditions imposed by the Municipality complied with, the property may not be utilised for any purpose other than the existing zoning.

In certain cases it is imperative that the Title Deed relating to the property be thoroughly examined in order to ensure that the intended use is not prevented by way of conditions contained in the Title Deed. Notwithstanding the fact that a Municipality may have approved the rezoning of a property, such property may still require the removal of a condition in its Title Deed. In certain instances this is achieved by way of an Application to the High Court. However in the majority of cases Title Deed conditions are removed by way of an application in terms of the Removal of Restrictions Act.

As with any application it follows that such application may be unsuccessful in which case the property would not serve the purpose for which it was purchased notwithstanding the zoning thereof.

In specific cases it is necessary for a further examination to take place over and above the reflected zoning.

Zoning Scheme Regulations invariably provide for a number of Use Zones and each Use Zone provides for Primary Uses which reflect the permitted usage under the applicable Use Zone. However in certain cases it is necessary for a further application to be made to the Municipality in order to utilise the property for a secondary use which is accommodated by the prosecution of a special consent or departure application to the Municipality.

It is therefore necessary that the intended use of a property be supported by either the use permitted in terms of the Primary Use or, alternatively, in terms of a further special consent/departure approval enabling the property to be utilised in terms of the required Secondary Use. Again, knowledge of the contents of the Zoning Scheme Regulations is required in order to examine whether the property will be capable of being utilised for the intended reason.

Property owners are able to obtain an Informal Town Planning Inquiry printout enabling them to ascertain the zoning which has been accorded to the property by the Municipality. However a detailed examination of Municipal records and the Title Deeds is advisable.

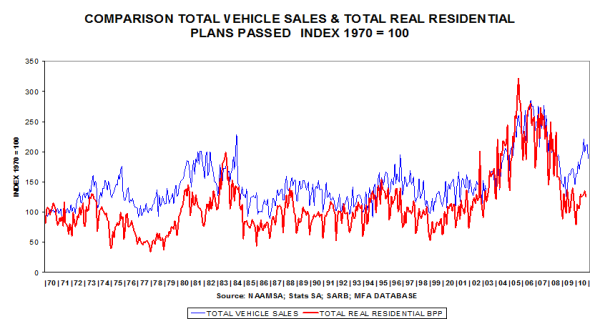

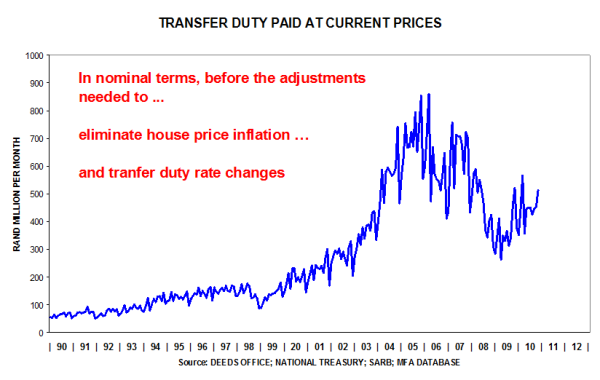

Vehicle sales are buoyant, but house plans are lagging.

The sharp improvement in house plans passed is taking a breather.

The level, in nominal terms, is recovering.

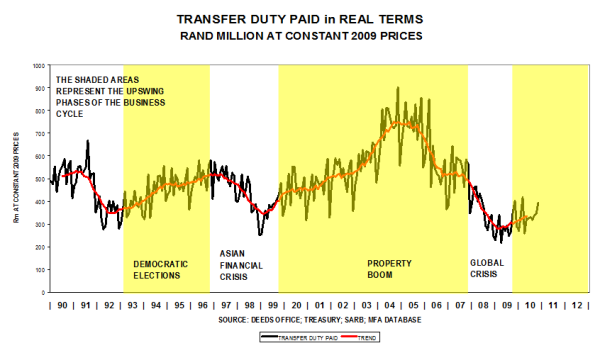

After eliminating inflation, the real level shows a steady improvement.

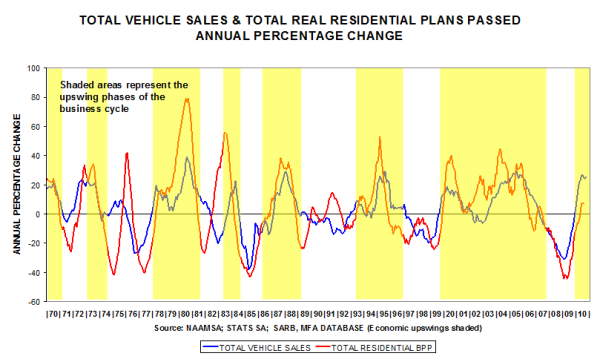

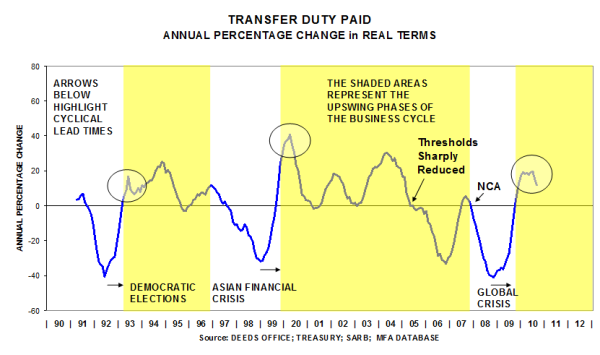

The annual percentage movement is conforming to pattern … first, rising rapidly, then moderating during the early part of the growth phase (refer circles).

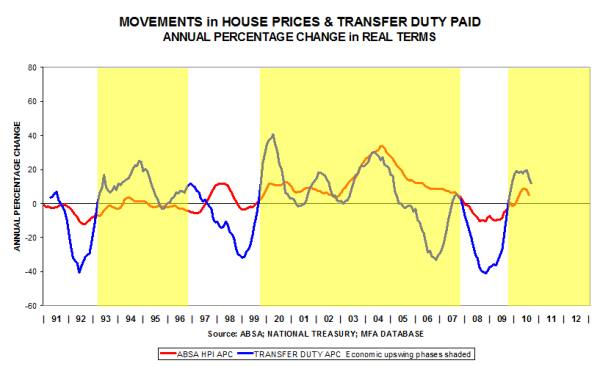

House price movements feed into the values of property transactions, on which transfer duties are based, hence the correspondence in cyclical movements. The activity series is more volatile than the price series because of significant changes in the underlying numbers of property transactions.

Most people are aware that there are certain costs involved in the purchasing or selling of a property. These costs can change depending on the entity that is used to buy the property in. This article will discuss the various cost items that typically affects a property transaction in South Africa.

Costs to the Purchaser

Attorney (Conveyancer’s) Fees

The first cost item to consider when buying a property is the conveyancing (attorney) fees. Although the purchaser pays the Conveyancer’s fee, it is usually the seller who appoints the attorney. This ensures that the conveyancer acts in the Seller’s interest and prevents unnecessary delays in the transfer process.

The conveyancer’s fee is paid for his/her role to change the ownership of immovable property from the Seller to the Buyer in accordance with the Deed of Sale.

Conveyancing Fees are prescribed by the Law Society of South Africa and is calculated on a sliding scale based on the purchase price of the property.

|

Value of property |

Recommended Guideline of Fees for |

|

R80 000 or less |

R3 200,00 |

|

Over R80 000 up to and including R90 000 |

R3 400,00 |

|

Over R90 000 up to and including R100 000 |

R3 650,00 |

|

Over R100 000 up to and including R125 000 |

R3 750,00 |

|

Over R125 000 up to and including R150 000 |

R3 900,00 |

|

Over R150 000 up to and including R175 000 |

R4 200,00 |

|

Over R175 000 up to and including R200 000 |

R4 400,00 |

|

Over R200 000 up to and including R250 000 |

R4 800,00 |

|

Over R250 000 up to and including R300 000 |

R5 500,00 |

|

Over R300 000 up to and including R350 000 |

R5 900,00 |

|

Over R350 000 up to and including R400 000 |

R6 400,00 |

|

Over R400 000 up to and including R450 000 |

R6 900,00 |

|

Over R450 000 up to and including R500 000 |

R7 500,00 |

|

Over R500 000 |

R7 500,00 for the first R500 000 plus R1000,00 |

A question that is often asked, is why the cost of a transaction increases with the property price when to all intents and purposes, the same amount of work is done. The answer to this lies in the risk that the Conveyancer assumes when he/she agrees to the transfer of a property: the greater the selling price, the greater the risks associated with the transaction.

Property Search Fee

The conveyancer has to do a Deed Search to ensure that there are no conditions in the title deed that prevents the proposed nature of the transaction. This is a fairly involved process as in many cases Title Deeds may refer to conditions in prior Title Deeds. For more information on this practice, refer to Meyer de Waal’s article on conditions “behind the pivot deed” published earlier in this blog.

The typical cost to do a Property Search range from R75 to R200 plus VAT.

Postages and Petties

Postages and Petties includes (but is not limited to) telephone costs, postage and courier fees, administration fees and bank charges. As a rule, the Transferring Attorney can recover any direct costs associated with the transfer of a property, but in reality it is often difficult to calculate the exact amount applicable to a specific transaction. Thus an estimate is used. Firms usually charge between R250-00 and R700-00 plus VAT for Postages and Petties.

FICA

With the introduction of the Financial Intelligence Centre Act in 2001, it became compulsory for all persons listed as Accountable Institutions in the Act to establish and verify the identity of any client prior to establishing a business relationship with such client. These include requiring a proof of residential address, the verification of the Identity Documents of the client and an in-person identification of the client. All documents pertaining to such verification must be stored for a period of at least five years.

The cost of a FICA verification varies between R200-00 and R550-00 plus VAT.

Electronic Generation Fees

Not all attorneys charge for Electronic Generation Fees, but nowadays this practice is quite common. This charge is usually disbursed to the purchaser when the Conveyancing Firm makes use of the Transactional Billing option that is offered by many Software Vendors. The Firm pays a fixed amount per set of documents that is generated with the software and this is passed on to the purchaser. The cost of Electronic Generation Fees for Transfers is usually around R150-00 per instruction plus VAT.

Rates Clearance

The conveyancer must obtain a Rates Clearance Certificate from the Local Authority to verify that there are no outstanding Rates and Taxes payable by the Seller. The municipality will not issue a Rates Clearance Certificate before all outstanding monies are paid. The cost of a Rates Clearance Certificate is currently R165-00, depending on the Local Authority.

Provisional Rates and Taxes

The purchaser will have to pay all rates and taxes 4 months in advance before the registration of the property can take place, but can claim a refund from the council for any amount paid, which is attributable to the rates due, following the registration of the Transfer.

Deeds Office Fee

The Deeds Office’s Fee for transferring a property is calculated on a sliding scale based on the purchase price of the property and is published in the Government Gazette from time to time.

|

Value of property |

Deeds Office Fee |

|

R150 000 or less |

R70,00 |

|

Over R150 000 up to and including R300 000 |

R350,00 |

|

Over R300 000 up to and including R500 000 |

R550,00 |

|

Over R500 000 up to and including R1 000 000 |

R650,00 |

|

Over R1 000 000 up to and including R2 000 000 |

R850,00 |

|

Over R3 000 000 up to and including R5 000 000 |

R1 050,00 |

|

Over R5 000 000 |

R1 250,00 |

Transfer Duties

Transfer Duty is a Tax that is levied by the Government on property transactions that depends on the Entity that buys the property.

For Natural Persons the tax is calculated on a sliding scale based on the purchase price of the property:

|

Value of property |

Transfer Duty |

|

From R0 up to and including R500 000 |

R0,00 |

|

Over R500 000 up to and including R1 000 000 |

5% of the amount above R500 000,00 |

|

Over R1 000 000 |

R25 000,00 + 8% of the amount above |

For Legal Persons (Close Corporations, Private and Public Companies and Trusts), transfer duty is calculated at a flat rate of 8% of the purchase price.

Entities that are registered for VAT can claim Transfer Duties paid back from the South African Revenue Service (SARS), but must levy VAT on top of the sale price when they sell the property again.

A Seller registered for VAT can sell a property as a going concern to Purchaser who is also registered for VAT and then a zero vatable transaction can occur. SARS recently published a memorandum on zero VAT transactions. Contact Meyer de Waal on 021 461 0065 for more information.

Home Owners Association Consent and Admin Fee

It is often a condition of the Local Authority that properties in Home Owners Association (HOA) may not be transferred without the consent of the Home Owners Association. This prevents the situation where a property can be transferred to a person who has not bound himself to the rules of the Home Owners Association. The cost levied differs from one HOA to the next, but typically is around R1000-00 plus VAT.

Costs to the Seller

Beetle, Electrical and Gas Conformity Certificates

The seller is obligated to give the buyer an electrical compliance certificate and is liable to pay the cost of any repairs to the electrical installation. Cost: Approximately R375.00

Although it is not compulsory to provide for a beetle-free certificate in a deed of sale, most financial institutions require a certificate before granting a home loan. The seller usually pays the cost associated with such an inspection. Cost: Approximately R375.00

Since 1 October 2009 any property with a gas appliance must be issued with a certificate of conformity. This must be issued by an authorised person registered as such with the Liquefied Petroleum Gas Safety Association of Southern Africa (LPGAS). You can read more on this requirement here. Cost: Approximately R150.00

Capital Gains Tax

Sellers have to pay capital gains tax on a property when it is sold. A capital gain (or loss) is the difference between the base cost of an asset and the net selling price upon the disposal of the asset.

For Natural Persons disposing of their primary residence, the first R1 500 000,00 of the Capital Gain is not taxable where after 25% of the gain is taxed at the individuals marginal tax rate.

For Legal Persons, 50% of the Capital Gain is taxable at the applicable entity’s tax rate.

For an accurate calculation of Capital Gains Tax, click here.

Estate Agent Commission

If a seller employs the services of an estate agent, the amount of commission negotiated will be payable by the seller on the registration of the transfer of the property. Commission usually varies between 3% and 7.5% (excluding VAT) of the selling price of the property.

Bond Cancellation Costs

If a bond is cancelled, the bank may require a three month notice of the seller’s intention to do so. If the seller fails to do this, the bank may charge interest for up to three months.

The fee paid to the attorney of a bank for the cancellation of an existing bond is +/- R 1 600.00.

Should you consider depositing your bonus into your bond account? The answer is undoubtedly yes!

If we assume that you get a bonus of R15 000 and that a bond of R500 000 is financed over 20 years, you can save almost R70 000 in interest and reduce the term of your loan with 1 year and 6 months! This is for a once-off sacrifice of R15 000!

If you do this every year until your bond is paid off, you will cut down the pay-off time with 9 years and save R303 000 in interest.

To do this calculation for your own circumstances, visit the FireFly Increased Instalment calculator.